Blog posts

The numbers describe a steep climb: eMarketer’s December 2025 forecast puts for example US in-store retail media ad spending up 33.1% in 2026 — even thoughin-store yet represents only a small sliver of the omnichannel retail mediamarket. The growth curve is real, and the channel is very early.

With that growth has come a sensible consensus: in-store cannot scale on manual operations. You cannot run a data-driven, outcome-based channel on static playlists and hand-built schedules, so the industry has rightly turned to automation. But the way automation usually gets framed — making inventory programmatic, bookable, and measurable so brands and agencies can buy it — describes only part of the problem. It automates the slice of in-store retail media the market talks about most, while much of what actually plays on the screens is handled somewhere else, by hand.

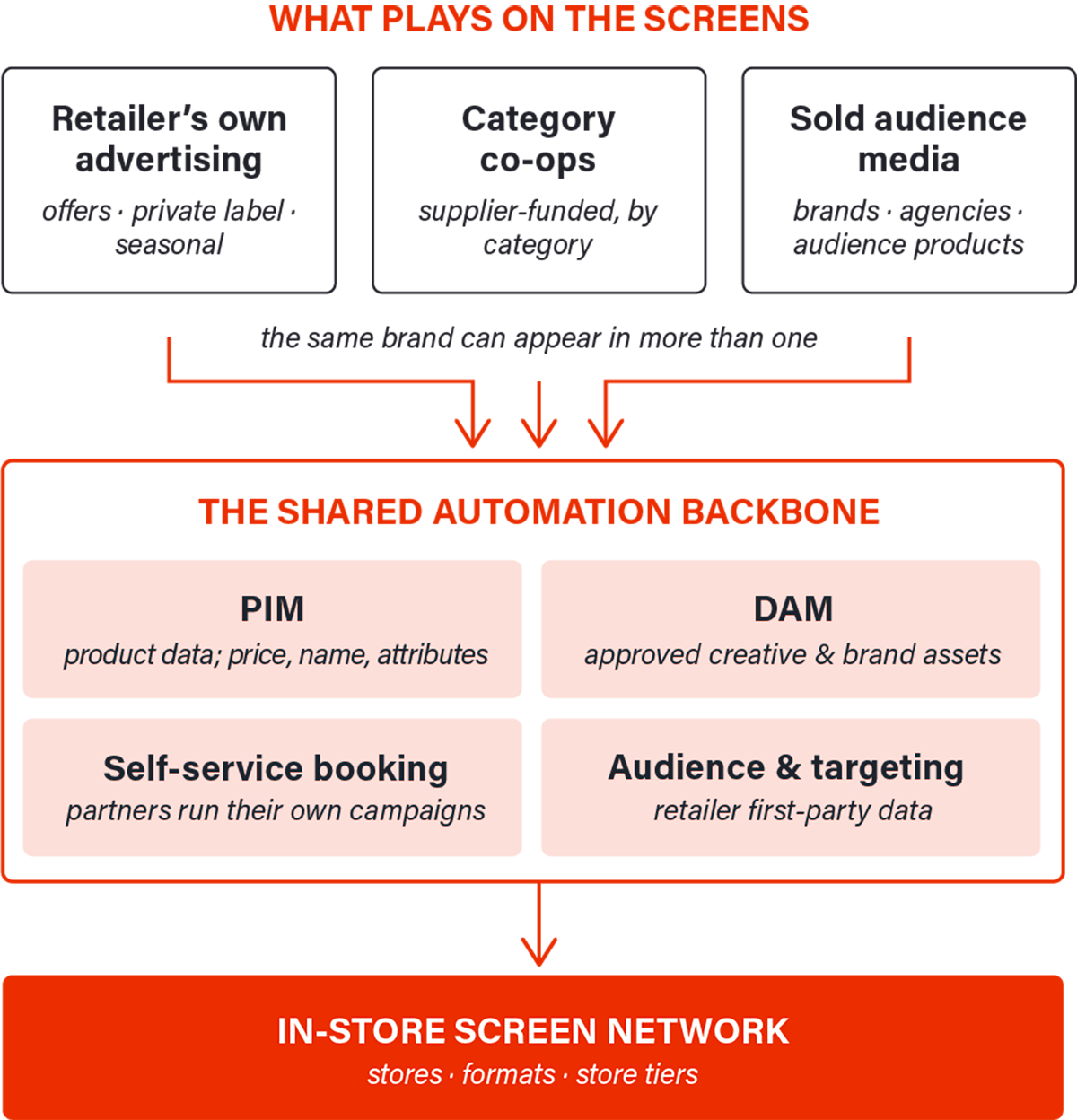

Because when you operate screens across a major retailer’s estate, sold audience media is one of several things running side by side. Alongside it sit the retailer’s own advertising and the tactical, category-level co-ops it runs with its brand suppliers, and today those still account for a large share of what plays. Sold audience media is the fastest-growing of the three — but it does not replace the others so much as join them; all of them co-exist on the same screens. Automate only the sold-media layer and a great deal of the operation is still being run manually.

Three kinds of advertising share an in-store network, and the lines between them are softer than an org chart suggests.

The first is the retailer’s own advertising: weekly offers, private-label pushes, seasonal campaigns, loyalty messaging, and store or service communications. This is driven by the retailer’s own promotional calendar and is priced and assorted according to the merchandising plan. It changes every promo cycle, and it differs by store format and region.

The second is co-operative advertising with brand suppliers — the tactical, category-by-category campaigns that are negotiated and funded jointly. A coffee supplier co-invests in the coffee aisle around a launch; a beverage category co-funds screens through a seasonal peak. These deals are frequent, granular, and tied to trade and promotional calendars.

The third is sold audience media: the audience-based products that brands and agencies buy, directly or programmatically. It is the part of in-store retail media that gets written about, and it is growing the fastest of the three.

These categories are useful for planning, but they blur in practice. The same brand may manage a co-op campaign itself through a self-service channel and, separately, buy audience products from the retailer’s media team for a national push. A single seasonal activation can be part retailer-funded and part supplier-funded. What matters operationally is less which box a campaign sits in than the fact that all of them land on the same screens and draw on the same underlying content.

It is worth noting where the market is heading on this point. eMarketer reports that in 2026 retailers are restructuring their retail media teams to sit closer to the functions that control pricing, assortment, and promotions — precisely the engines that drive a retailer’s own advertising and its category co-ops. The organisational centre of gravity is moving toward the relevant content that fills the screens, not only the media-sales storefront on top.

The reason this matters for automation is that the content behind these campaigns is not ad creative sitting in a media plan. It is product data and brand assets that mostly already live in the retailer’s systems.

Prices, product names, pack shots, and attributes live in the Product Information Management system — the PIM. Approved campaign and brand creative lives in the Digital Asset Management system — the DAM. A weekly category promotion is, in practice, a query against those two systems: take this product, at this price, with this image, render it to this template, on these screens, for this flight.

Done by hand, that means exporting a price list, retrieving the right pack shots, rebuilding a template per category and per store tier, and re-checking all of it when the price changes on Thursday. Multiply by hundreds of promotions a week, across dozens of categories and thousands of stores, and the process does not just fail to scale — it fails on accuracy, and a wrong price on a screen is worse than a dark one. The co-op layer stacks a commercial workflow on top: each deal carries its own funding, approvals, and dates. Run that in spreadsheets and email and the operational cost quietly consumes the revenue it was meant to capture.

So the real automation question for in-store retail media scaling up is not “when can we make the inventory programmatic?” It is “is the screen network wired into the systems where the retailer’s content and product data already live?”

With PIM integration, product data flows straight into dynamic templates: a price, a name, or an image is changed once, at the source, and it is correct everywhere it appears. A category promotion becomes a data-driven template rather than a hand-built artboard. With DAM integration, approved assets move automatically, so a campaign always uses the right creative and inherits updates from the source of truth. And a self-service layer lets trade and category partners manage their own campaigns — the booking, the asset supply, the approvals — within the retailer’s own guardrails, rather than as a manual service the retailer has to staff.

That same pipeline is what makes the sold-media layer trustworthy, too. The integration that keeps a private-label promotion accurate is the integration that keeps a paid brand campaign accurate — and, often, that paid campaign is the same supplier who books a co-op slot through self-service the following week. Get the backbone right and the audience products the market is so focused on become the straightforward part. Integration, in other words, is not a feature you bolt on once a media-sales motion exists. It is the foundation the whole operation stands on.

The market is moving in-store retail media from experimentation toward disciplined, repeatable execution, and pulling retail-media teams closer to pricing, assortment, and promotions. That shift only pays off if the platform reaches into the systems where those decisions are already recorded. The retailers who scale in-store will not be the ones who bought the slickest media-sales front end. They will be the ones who automated all of it — their own promotions, their category co-ops, and their sold media — on top of the content and product data they already own.

This is the premise we build on at Doohlabs. In-Store IMPACT integrates with the retailer’s DAM and PIM and gives trade partners a self-service booking layer, so the entire content operation — not just the sold slice — runs from the data and systems the retailer already controls.