Blog posts

In-store retail media has moved past the pilot phase. Retailers across Europe and North America are now building serious networks — more screens, more formats, more stores, with retail media written into the business case from day one. As the scale of these investments grows, the question that used to dominate every planning meeting — where we should put the screens — is quietly being replaced by a harder one.

Every screen in a modern retail environment is being asked to do three different jobs at the same time. It carries paid retail media for external advertisers. It hosts trade-partner co-op campaigns with the retailer's suppliers. And it runs the retailer's own marketing — promotions, loyalty programmes, brand messaging. These three jobs share the hardware but very little else from a marketer's perspective. They sell at different prices, are measured on different KPIs, and respond to different creative. Treating the entire fleet as one undifferentiated pool is the easiest way to underprice the best inventory, overpromise on the average, and quietly subsidies the rest.

The work of the operating team — and of the analysis that supports it — is to decide, screen by screen, which of the three jobs each one performs best. The methods that lead to a defensible answer depend on where the network is in its lifecycle. Three stages of maturity each call for a different toolkit.

At this stage, the screens have not yet been installed. The strategic decision has been made — retail media is a genuine line of business, and the network will be designed around it — but everything still lives on a floor plan.

The instinct here is to place screens where customers will see them and resolve the commercial model afterwards. That sequence creates the misclassified networks that the next two maturity levels spend years correcting. Designing the network around the commercial model from the outset is significantly cheaper than retrofitting one later.

Because there is no impression data yet, the analysis at this stage is necessarily structural. Three methods do most of the work. The first is a series of structured store walkthroughs, with merchandising, marketing and — where the function already exists — retail media in the room together, mapping the shopper journey and assigning a primary job to every prospective screen location before the hardware is ordered. The second is footfall and dwell pattern modelling drawn from whatever data the retailer already has — till counts, counter logs, loyalty traffic — to estimate which zones can carry a media-grade audience. The third is peer benchmarking against comparable networks elsewhere, typology by typology rather than chain by chain, so that the placement plan starts from a realistic view of what entrance gates, main aisles, end-caps and checkout screens deliver in practice.

The role decision at this stage is also structural. Entrance and main-circulation screens tend to be designed as retail media inventory: they reach every shopper, they are easy to audit, and they are the most straightforward sell to a CPG media buyer. Category-aisle and end-cap screens tend to start life as trade co-op territory, closer to the shelf and with a clearer line of sight to category sales. Shelf-edge, cashier and back-of-store screens are usually designed for the retailer's own marketing, closer to product information than to media. None of these classifications is permanent, but the role each screen is designed for is the one whose data, two years from now, will be the easiest to defend.

This is where most retailers currently sit. The screens have been in place for years, installed for own promotions, trade marketing or even wayfinding. The strategy has now been upgraded — this is a retail media business — but the fleet underneath was not fully designed for it, and the operating layer is being asked to do two jobs on platforms built for one.

The task at this level is re-classification, and unlike the previous stage, the data finally exists to do it properly. Walkthroughs and store-team hypotheses remain useful, but they are no longer sufficient on their own: too many of the original decisions were made for a different purpose, and the people who made them are not always still in their roles.

The methodology that does the heavy lifting at this stage is anonymous computer-vision audience measurement. The technology has matured considerably. Modern systems perform body and face detection rather than recognition, generate no biometric templates, do not re-identify shoppers across appearances, and operate squarely within GDPR's Anonymous Video Analytics framework. What they deliver is per-screen impressions, demographic segment composition, dwell and attention time, and exposure-zone reach — the operational inputs that turn a fleet of screens into a priced inventory.

Where the retailer holds eye-tracking data on attention, that input remains genuinely valuable. It describes how a shopper processes a screen once they are right in front of it and especially how their attention differs when contents changes. Peer benchmarking against grocery, convenience or non-food peers then tells the retailer whether the numbers it is seeing are competitive or only internally consistent.

This is the level at which the role decision becomes a live commercial conversation. A screen originally installed to promote the loyalty content may turn out to deliver a more attractive audience than expected and earn its way into the retail media inventory. A category-aisle screen the supplier already funds via trade marketing may overlap with a paid campaign aimed at the same audience. The objective is not to settle the role question once and for all. It is to make the question visible — and to price the answers.

This is the level the most advanced retailers have reached. The network is operational. Campaigns are running. Trade co-op and retail media sales both move through the same system. The question has shifted again, from where should screens go to how much of what we already have are we monetizing correctly.

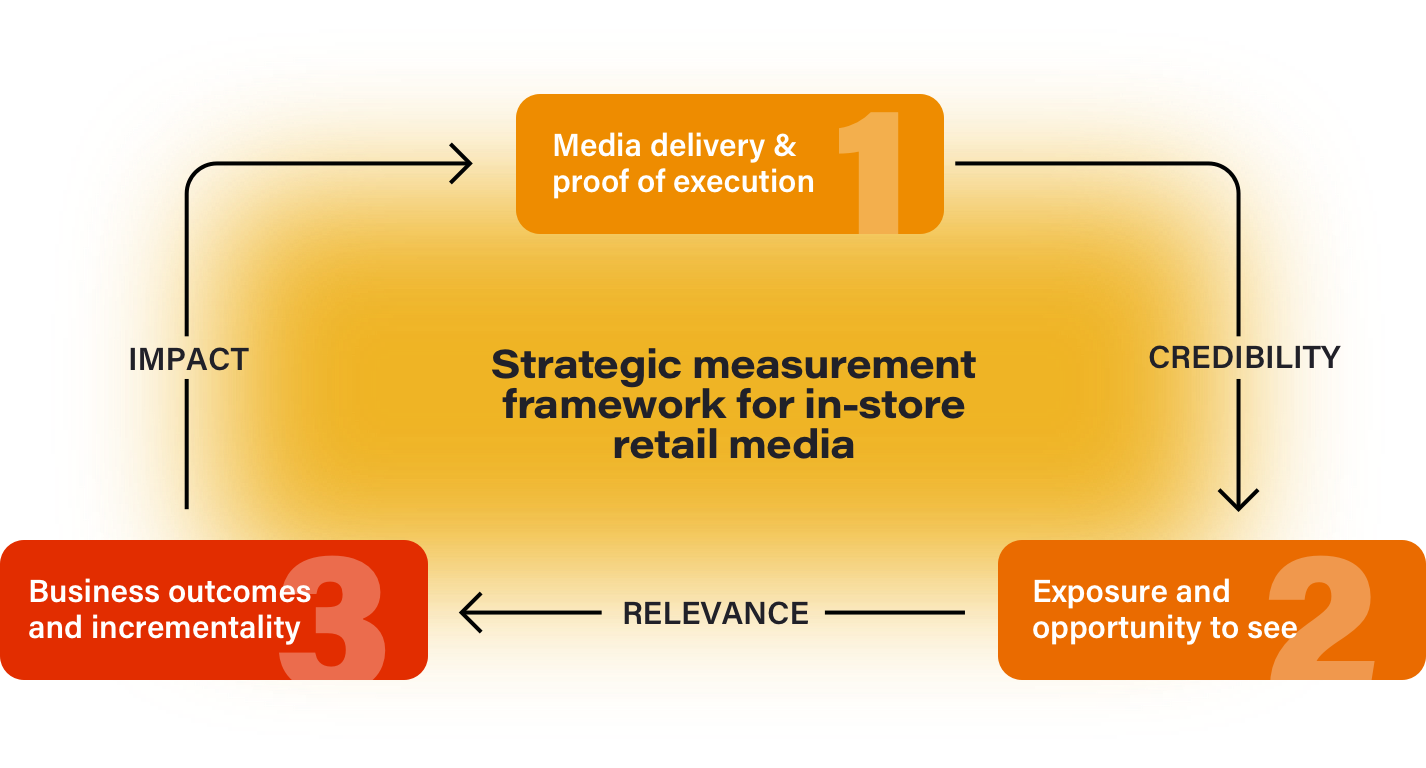

A useful frame at this stage is a three-level measurement model. Credibility covers media delivery and proof of execution — the unglamorous but essential evidence that a campaign ran where and when the buyer paid for it. Relevance covers exposure and opportunity-to-see — who was in front of the screen, when, and for how long. Impact covers business outcomes and incrementality — the closed-loop link between media exposure and sales, basket and loyalty data. Each layer earns the next. An advertiser will not engage with an incrementality story if the proof-of-play underneath it is sloppy.

The methodology stack at this level is the widest of the three. Structured before-and-after measurement is the core: baseline the existing placements with computer-vision sensors, reposition selectively on the back of the findings, then measure again and compare per screen and per zone. A typical project of this kind runs across two or three reference stores per format, several weeks per phase, with a sample size sufficient to support statistically defensible conclusions per instrumented screen.

Around that core sit four supporting analyses. Daypart and peak-window analysis turns aggregate impressions into accurate pricing — a Sunday afternoon at the entrance gate is not the same product as a Wednesday morning in the dairy aisle. Demographic-segment profiling reveals which screens reach which audiences, and which do not, regardless of how heavy their footfall is. Content A/B testing identifies which creative formats earn their time on the screen, by segment. And the closed-loop link to POS, loyalty and SKU sales finally allows the retailer to describe what each screen contributes, not merely what it shows.

This is also where the role decision is re-answered with evidence. A screen long sold as retail media inventory whose closed-loop lift is consistently weak may be more valuable re-allocated to trade co-op, where category proximity is what the buyer is paying for. A trade screen with an unexpectedly broad and engaged audience may be reclassified upward into the media pool. Optimization, at this level, is not about moving screens. It is about reassigning roles on the basis of what the data actually shows.

The temptation, at every level of maturity, is to skip the role question and let the market resolve it commercially. It unfortunately rarely does. A network in which every screen is doing some unclear blend of three jobs will see its best inventory subsidizing its worst, its CPMs settling at the mean, and its advertisers — external brands and trade partners alike — eventually asking why the numbers do not match the promises.

The retailers who compound through the next phase of in-store retail media will be the ones who design the role question into the network from the start, and who keep asking it as the data improves. The methods that answer the question change with maturity. The discipline of asking it does not.