Blog posts

In-store retail media has stopped being a side experiment long ago — it has become a stated strategic priority for retailers all over the world. Brands have come to expect closed-loop reporting and audience-grade targeting as the new baseline. Kroger and Albertsons are aggressively rolling out their in-store screen networks; Tesco and other Europeans have been at it for years.

And yet, somewhere inside almost every in-store retail media network, the master file that governs all of it is still called inventory_master_v17_FINAL_FINAL.xlsx.

That file used to be just a productivity drag. Today it has become a commercial drag — and of course, it is not the actual problem.

When in-store retail media operators run their inventory in Excel, it is rarely a question of laziness or budget. It is a question of what is underneath. The operating layer in most networks has been built up in three sediments — none of which were originally designed for the job at hand.

The first sediment is a basic digital signage system, inherited from the era before any of this was a media business. Its purpose, of course, was to schedule playlists and push content to screens. That is a playback problem and not a media-sales problem. A basic signage system can tell you what is playing on the screen at 4:17 pm in store 412, but it cannot tell you in real time how full the network is, which audience pockets are oversold, or what you can responsibly promise to a buyer for next Tuesday.

The second sediment is the decision to enter retail media without changing that operating layer. The strategy got upgraded; the platform did not. The same screens that used to run own-promotions are now expected to deliver audience-grade campaigns to paying advertisers, but the system underneath still treats them as plain playlists.

The third sediment is Excel, layered on top. When the signage system cannot answer the commercial questions, and no platform was put in to replace it, the planner reaches for a spreadsheet. The spreadsheet cannot really answer those questions either, but at least it lets you pretend.

This pattern is identical whether the network is run by a retailer’s in-house retail media team or by a media sales company on an outsourced basis. So is the cost. Most operators do not really know in detail how full their inventory is, and they do not know precisely what should be sold at each moment to fill it.

This shows up in many ways, and all of them have a price tag.

You sell less than you actually have. When the spreadsheet is ambiguous, the team turns down deals “to be safe”. This means real revenue left on real screens on real days, against imaginary scarcity.

You make promises you cannot always keep. A category gets oversold across two corners of the network and the overlap does not surface until after the fact. The advertiser underdelivers, the post-campaign report is awkward, and the renewal conversation never quite warms up. One bad delivery can cost you a relationship — not just a row in a sheet.

Monday morning, the team is blind. “Where are we under-pacing? Which advertisers crowd which audiences? Which stores can absorb a last-minute insertion order?” If the answer takes a meeting and two analysts, the network is being run reactively.

And of course, you cannot really grow into the strategy you already announced. You have already committed — to your board, to your owners, to yourself — to running in-store retail media as a real media business: many stores, many target groups, many advertiser categories. Excel collapses the moment that real business actually starts. It cannot model audience overlap, show pacing across selected store types, or reconcile a trade marketing spot and a paid media spot competing for the same shelf-edge screen at the same hour. The strategy does not fail because it was wrong. It fails because the operating picture stopped matching reality.

The advertiser sitting across the table is no longer the merchandising contact from five years ago. Today, they sit in the brand’s media team. They run campaigns in which audiences are defined upfront and post-campaign sales lift is reported back. And they have come to expect the same of in-store. They will ask which target groups your screen network reaches, in which stores, and with what overlap on competing brands. As global consultancy Oliver Wyman puts it in their analysis of retail media as a growth engine, the channel scales only when measurement, targeting and delivery match what brand teams already plan against.

When you answer those questions with a screenshot of a tab, two things happen. The advertiser stops seeing you as a media business. And that perception will show up in the next CPM negotiation.

There is a useful consensus forming in the field that in-store retail media should pivot from selling slots to selling audiences. We at Doohlabs agree, but only partly. The advice is right. It is also incomplete.

You cannot really sell audiences you cannot see.

If your operating layer is a basic signage system stitched to a spreadsheet, your inventory exists in the world as time on screen — not as which target groups are reachable, in which stores, when, and against which competing demand. In our view, the pivot to audience-based selling is a tooling change first and a sales-pitch change second. Anyone telling you otherwise is, of course, selling a slogan.

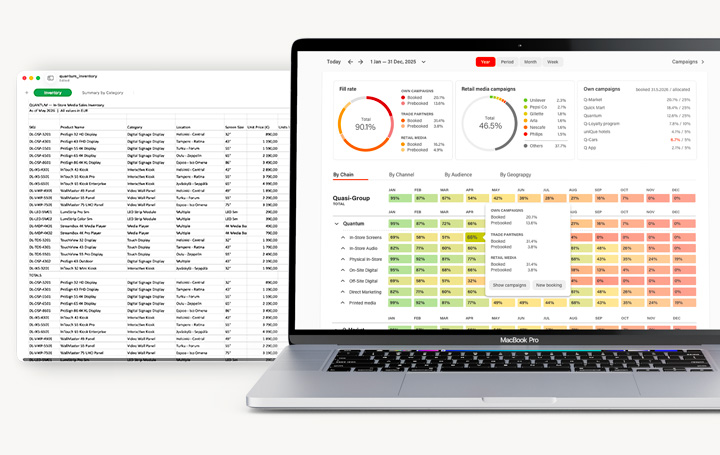

The retailers and media sales partners who will compound through the next five years of in-store retail media are the ones whose internal operating picture is as confident, real-time and defensible as the view their advertisers already have. They will know fill rate by audience and store, not just by aggregate. They will know what to sell next, not just what was sold last week. They will say yes to a deal — or hold a premium — at the speed the buyer expects.

That is the view we at Doohlabs have built. One operating picture across own campaigns, trade marketing and retail media sales — so that the helicopter view and the sales floor finally point at the same thing.

If the file that governs your network ends in _v17_FINAL_FINAL.xlsx, the cost of fixing it has finally dropped below the cost of keeping it.